You get a job offer with a CTC of ₹8 lakh, you do the quick mental math — about ₹66,000 a month — and then your first salary lands and it’s noticeably less. If that’s happened to you, you’re not alone. The gap between the CTC on your offer letter and the money that actually reaches your bank account confuses almost every new employee.

This guide explains exactly why that gap exists and shows you, step by step with a full worked example, how to calculate your real in-hand salary from your CTC.

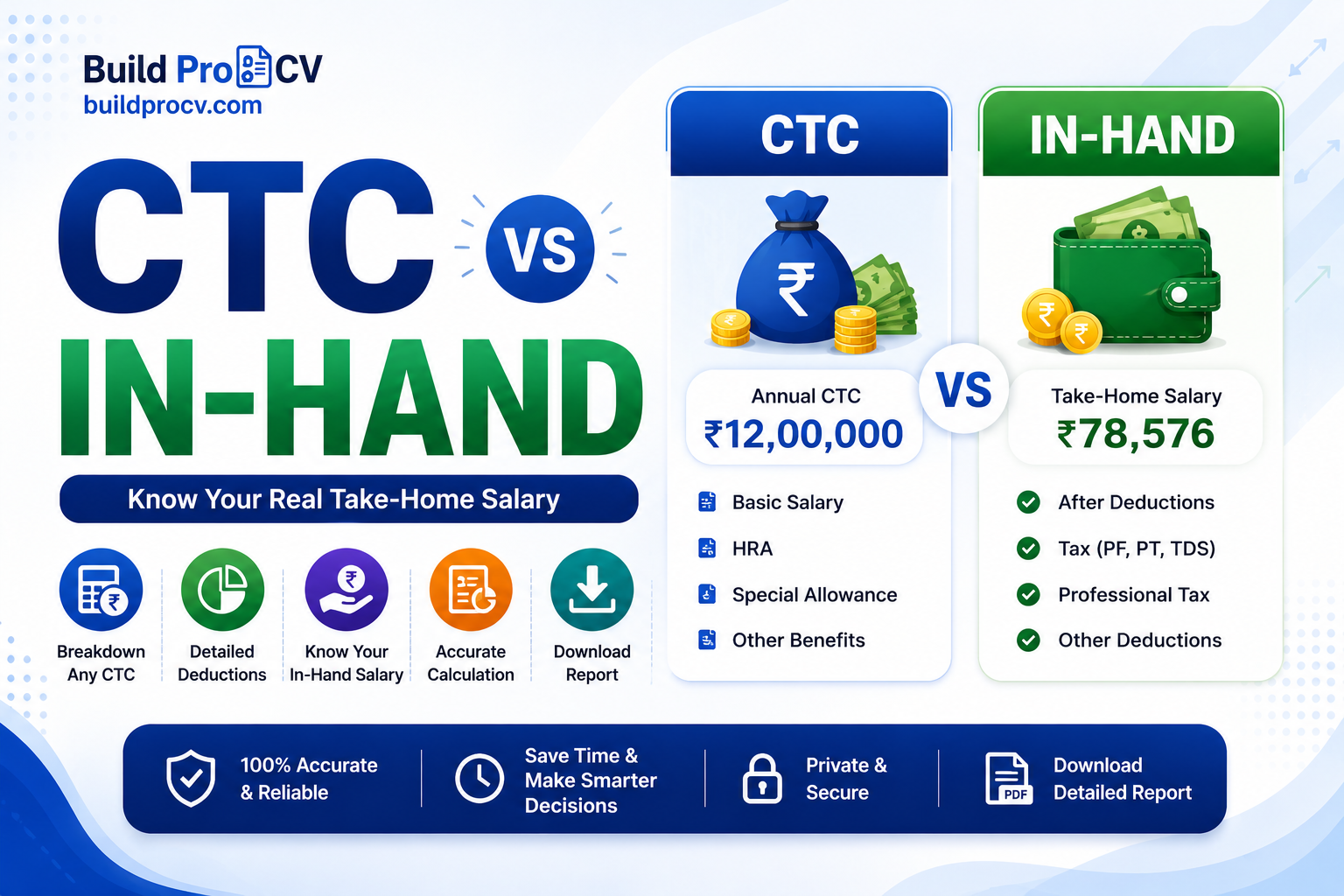

CTC vs in-hand salary: the quick version

CTC (Cost to Company) is the total amount a company spends on you in a year. It includes your salary plus everything else — the employer’s contribution to your provident fund, gratuity, and any benefits or bonuses.

In-hand salary is what’s actually credited to your bank account each month after all deductions.

The key thing to understand: a big chunk of your CTC never reaches you monthly. Some of it is the company’s contribution to your future savings, and some is deducted as tax and provident fund. That’s why your in-hand is always lower than CTC ÷ 12.

What’s inside your CTC?

Your CTC is usually made up of these parts:

Basic salary — The core of your pay, often 40–50% of CTC. Many other components are calculated as a percentage of this.

Allowances — House Rent Allowance (HRA), special allowance, conveyance, and others that top up your pay.

Employer PF contribution — The company puts roughly 12% of your basic salary into your Employees’ Provident Fund. This is part of CTC, but it goes into your PF account, not your monthly bank balance.

Gratuity — A retirement benefit set aside by the employer (around 4.81% of basic). It’s counted in CTC but you only receive it after completing several years of service.

Bonuses or variable pay — Performance or annual bonuses, which may or may not be paid out fully.

What gets deducted from your salary?

To get from CTC to in-hand, you subtract:

- Employer’s PF and gratuity — these are part of CTC but never come to you monthly, so remove them first to get your gross salary.

- Employee PF contribution — about 12% of your basic salary, deducted from your pay and added to your PF account.

- Professional tax — a small state-level tax, typically up to ₹2,500 per year (it varies by state, and some states don’t charge it at all).

- Income tax (TDS) — deducted based on your income and tax regime.

Step-by-step: how to calculate in-hand salary from CTC

- Start with your annual CTC.

- Subtract the employer’s PF contribution and gratuity → this gives your gross salary.

- From the gross salary, subtract your employee PF contribution.

- Subtract professional tax.

- Subtract income tax (TDS), if any.

- What’s left is your annual in-hand salary. Divide by 12 for the monthly figure.

Worked example: ₹8,00,000 CTC

Let’s run a realistic example. (Exact numbers depend on your company’s salary structure and your state, so treat this as an illustration.)

Starting CTC: ₹8,00,000 per year

- Gratuity (≈4.81% of basic): ₹15,392

- Basic salary (40% of CTC): ₹3,20,000

- Employer PF contribution (12% of basic): ₹38,400

Step 1 — Gross salary ₹8,00,000 − ₹38,400 − ₹15,392 = ₹7,46,208

Step 2 — Subtract deductions from gross

- Employee PF (12% of basic): −₹38,400

- Professional tax (approx.): −₹2,400

- Income tax: Under India’s new tax regime for FY 2025–26, salaried income up to about ₹12.75 lakh attracts effectively zero income tax thanks to the standard deduction and rebate. At ₹8 lakh, income tax here is nil.

Annual in-hand: ₹7,46,208 − ₹38,400 − ₹2,400 − ₹0 = ₹7,05,408

Monthly in-hand: ≈ ₹58,784

So a ₹8,00,000 CTC translates to roughly ₹58,800 a month in hand — not the ₹66,000 a simple division would suggest. The difference went into your PF (your own savings, just not spendable now), gratuity, and a small professional tax.

A note on PF: this example uses the standard 12% of basic. Some companies instead cap PF at ₹1,800 a month (the EPF wage-ceiling rule), which makes the PF deduction smaller and your in-hand a little higher. Our calculator lets you choose whichever matches your payslip.

A note on income tax: tax rules and slabs change from year to year and depend on whether you choose the new or old regime. Always check the latest slabs for the current financial year before relying on a tax figure.

The fastest way to find your in-hand salary

Doing this by hand is fine once, but if you’re comparing offers or just want a quick number, use the free CTC to In-Hand Salary Calculator. Enter your CTC, choose your tax regime, and it estimates your monthly take-home after PF, professional tax and income tax — and even compares the old and new regimes to show which saves you more. You’ll see your real number in seconds and can compare two job offers fairly instead of being misled by the headline CTC.

Frequently asked questions

Why is my in-hand salary less than my CTC?

Because CTC includes amounts that never reach your monthly account — like the employer’s PF contribution and gratuity — plus deductions such as your own PF contribution, professional tax and income tax.

How much of CTC is in-hand?

It varies with your salary structure, but in-hand is commonly around 70–85% of CTC for lower and middle income levels, with a larger gap at higher salaries due to tax.

Is PF deducted from CTC or salary?

Both. The employer’s PF contribution is part of your CTC, while your own (employee) PF contribution is deducted from your monthly salary. Both go into your PF account.

Does in-hand salary include HRA?

Yes, allowances like HRA are part of your gross and in-hand salary, though HRA can have tax implications under the old regime.

Is income tax always deducted from salary?

Not always. Under the new tax regime for FY 2025–26, salaried income up to roughly ₹12.75 lakh can be effectively tax-free, so lower earners may have little or no TDS. Higher salaries attract income tax as per the applicable slabs.